Level 2 Listening: listen for values and to the person – not to the actual problem. Listen to what matters most and not to the goal/outcome. DO NOT try to relate to the person speaking by sharing your own experiences. Just listen

Organizational Structure need to align with the company strategy

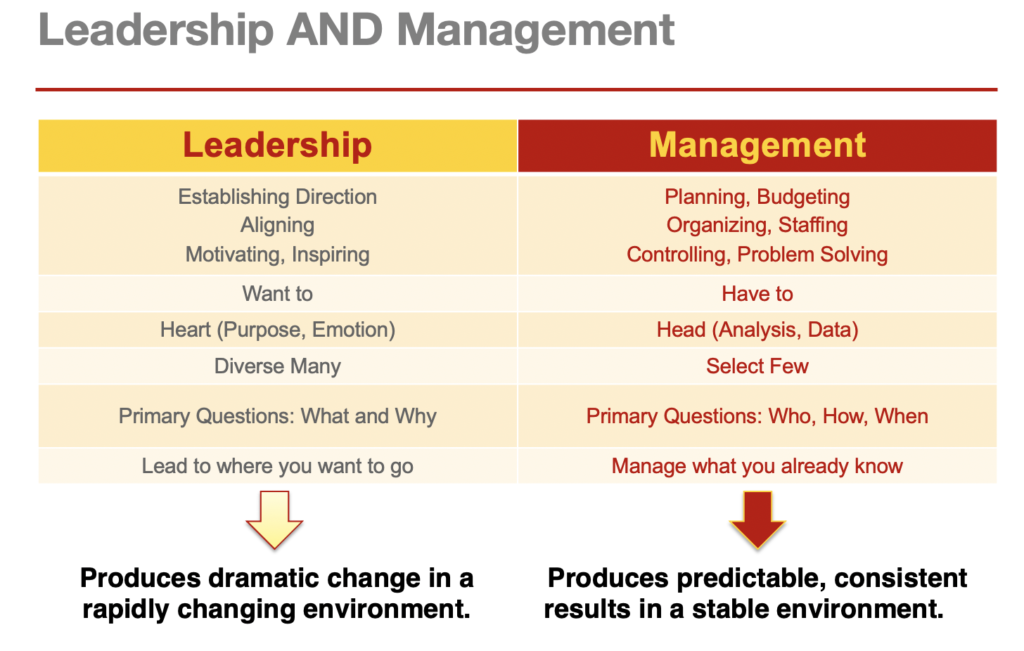

Keep things you want to do in the ‘want to’ – I’m doing it because I want to. If you move it to the ‘have to’ – I have to do it (because of pay or something) – it takes the fun out of it and I would probably stop doing it

In a crisis – go back to basics. Simplify and create clarity around what’s important to solve the problem – and what’s not

It takes 7 times for someone to hear something before they internalize it. It takes 30 times for someone to hear something to change their behavior

Leaders’ words matter!

When interviewing someone, listen to the stories people tell and how they connect together. Think about how the stories connect to each other, and see if there’s good connection. Ask questions like: ‘how did you get from story a to story b? What did you learn’?

Connecting with people on a value level is deep and can help bridge a lot of disagreements

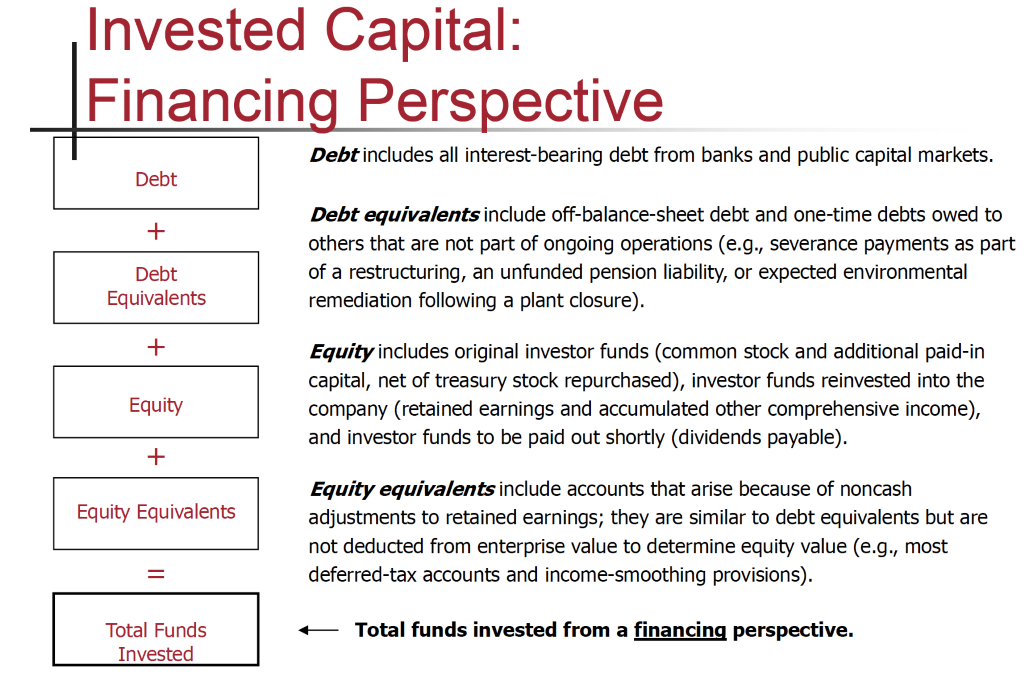

Accountants describes liability as a present contractual commitment to another entity that entrails settlement by probably future transfer or use of assets on an agreed upon date (or timing) when the obligating event has already occurred. There is no exact definition of debt in accounting, and not all liabilities are debt. Also, it is possible that some types of debt are not considered a liability by accountants (off-balance sheet financing).

DEBT

For our purposes, debt is an amount contractually owed to another party that has an explicit or implicit interest payment that we can measure. That includes notes, mortgages, bonds (debentures), and other financing instruments that typically have an explicit or implicit interest rate. That EXCLUDES liabilities such as deferred income taxes, unearned revenue, and most other operating liabilities (for example, accounts payable (AP), wages payable, accruals, etc.)

======================

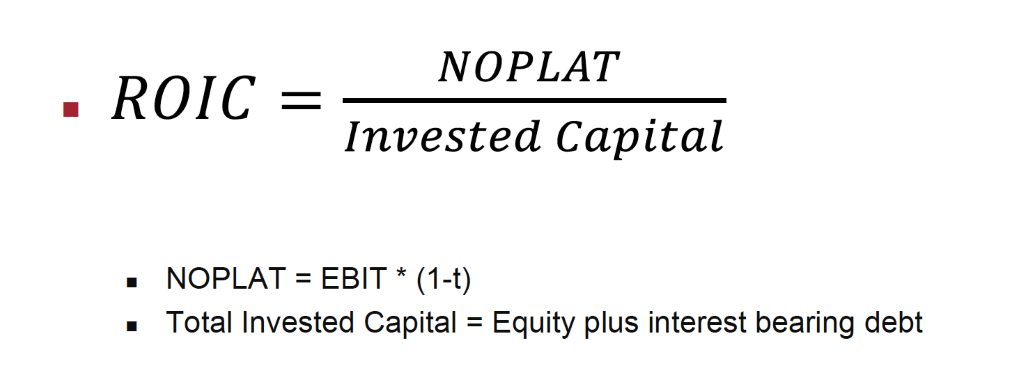

ROIC – Return On Invested Capital = NOPLAT/Invested Capital (=debt + equity) NOPLAT = Net Operating Profits After Tax (to get the tax rate = taxable income/tax expense) NWC (Net Working Capital) = current assets – current liabilities

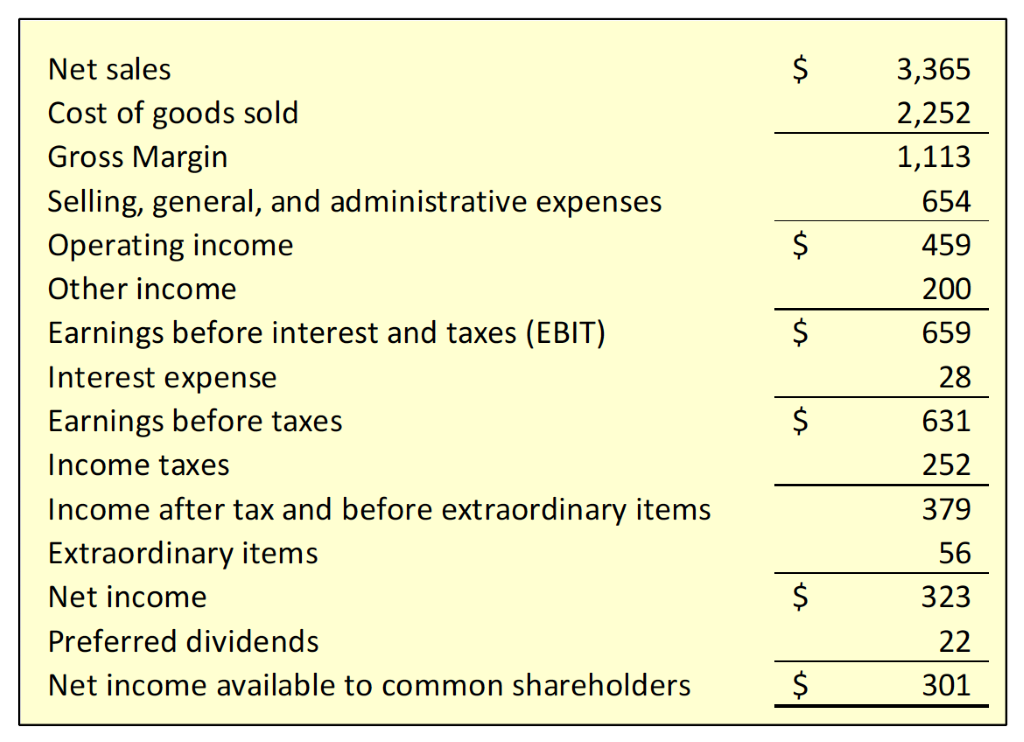

Income Statement: Operating income vs non-operating income – If we’re looking to value OPERATIONS ONLY, we’re stopping at the EBIT! After the EBIT come the financial performance. Operating Income: the income generated by the firm’s core business operations. Non-operating Income: income generated by investments the firm has made in assets that are unrelated to the firm’s primary business. For example:

Gains from the sale of investments

The sale of a subsidiary or division

Costs incurred from restructuring

Currency exchange

The write-off of obsolescent inventory

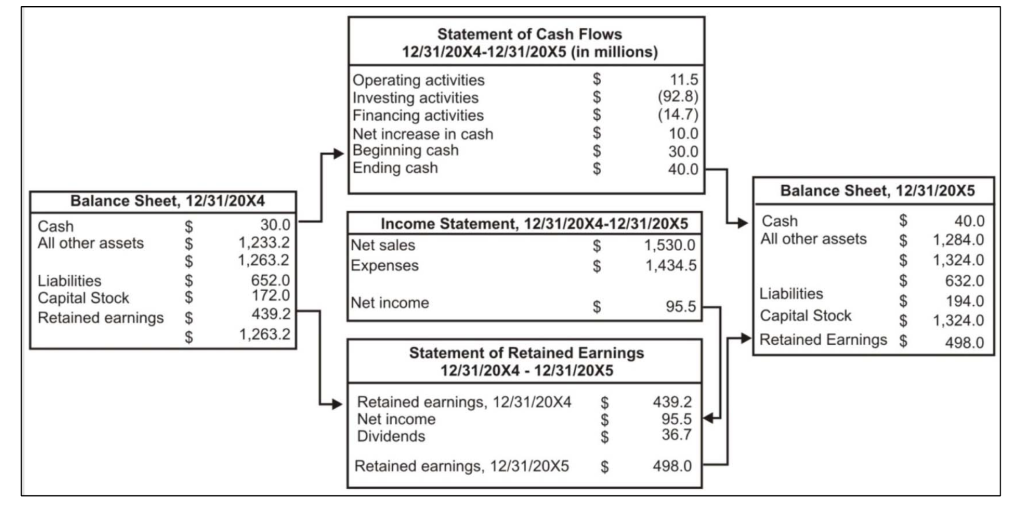

The Balance Sheet: provides a snapshot of the firm’s financial position at a moment in time and a detailed account of the company’s assets’ liabilities (debts), and shareholders’ equity. The balance sheet equation requires that the sum of the book values of the firm’s assets equal the sum of the debts the firm owes to its creditors plus the investment of the stockholders’ equity.

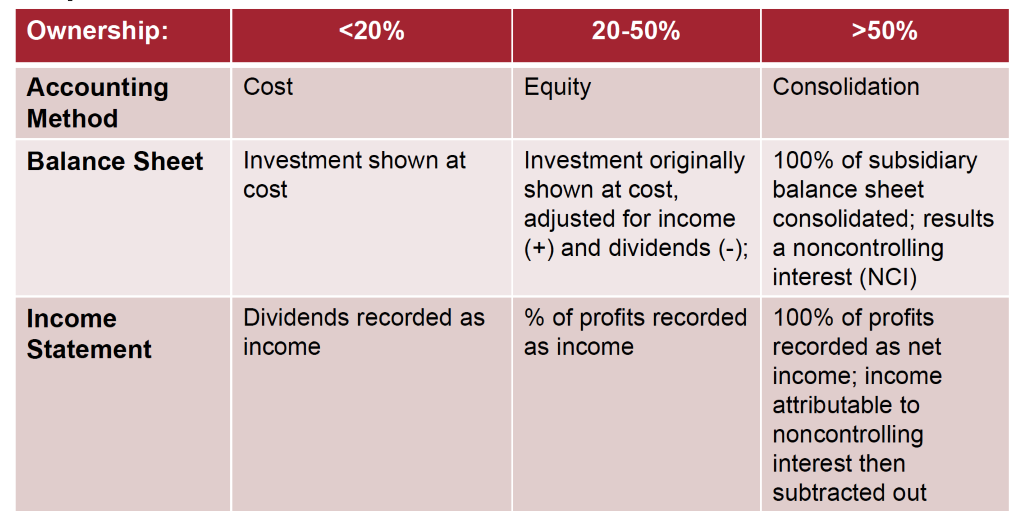

Consolidation Rules:

An equity investment involving more than 20% but less than 50% of the equity of another firm is recorded as an investment. This will typically show up on the balance sheet as ‘investments in unconsolidated subsidiaries’.

If the firm owns more than 50% of a subsidiary, then the rules of accounting call for consolidation of the subsidiary into the firm’s balance sheet and income statement. A minority interest account appears between liabilities and shareholders’ equity, representing the value of the minority-owned shares, because 100% of the value of the subsidiary’s assets were incorporated into the consolidated balance sheet.

The presence of a long-term investment category on a firm’s balance sheet signifies the presence of a potentially significant non-operating asset that will need to be valued. This means that the analyst will need to dig deeper into the footnotes of the financial statement to determine the exact nature of the investments in order to determine an appropriate approach to valuing them. This line item (sometime referred to as long-term investments because they are assets the company intends to hold for longer than one year) can consist of stocks and bonds of other companies, real estate, as well as cash set aside for a specific purpose.

Ratio Analysis

Categories of ratios:

Profitability Ratios

Profit margin (net income/sales)

Return on assets (ROA) = net income/total assets

Return on equity (ROE) = net income/total equity

Short-term solvency (liquidity ratios)

Current ratio (CA/CL)

Quick ratio (CA-inventory)/CL

Long-term solvency

Leverage ratios

Total liabilities to total assets (TL/TA)

Total liabilities to total equity (TL/TE)

Total assets to Owners’ equity (equity multiplier): TA/TE

Total debt to equity (TD/TE)

Coverage ratios

Times interest earned/EBIT interest coverage (EBIT/interest)

The longer inventory sits on a company’s shelves, the lower the rate of return on those assets, and the greater their vulnerability to falling prices and obsolescence. You want to keep your inventory turning, however not at the expense of your overall profit margins or business strategy

Benchmarking using ratios: so, what is a good benchmark?

It is often not clear what is a ‘good’ or ‘bad’ level for a financial ratio and no one benchmark exists for all companies in all valuation contexts. We know ratios vary over time and we know they vary by industry – we also know that companies tend to regress towards the mean – so a common benchmark is the company’s industry or comparable group. That said – deviations from the ‘norm’ might be good and indicate an industry leader and a potential competitive advantage.

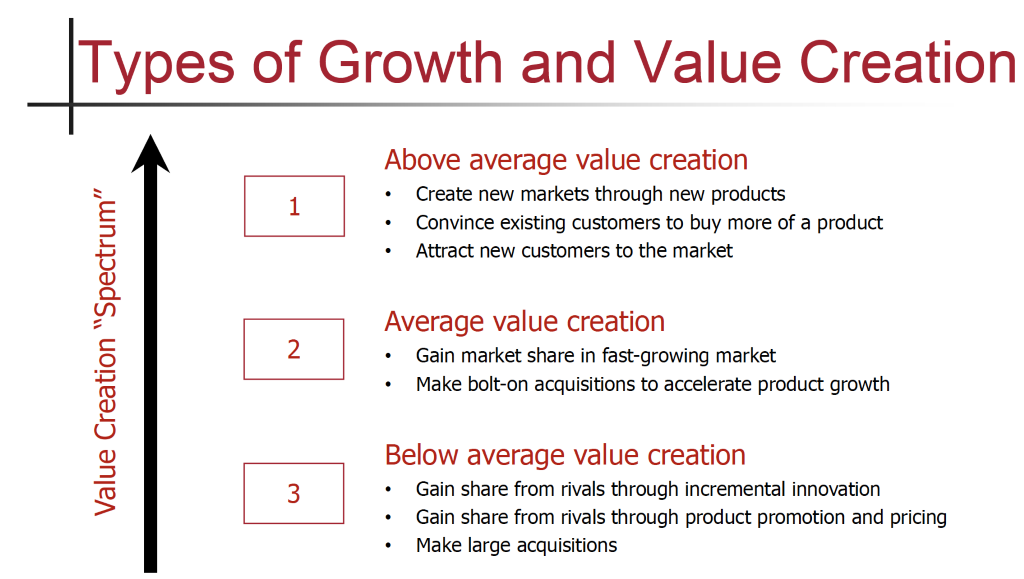

ales growth is an important driver of the need to invest in various types of assets and of the company’s value. It also provides some indication of the effectiveness of firm’s strategy and product development activities.

Analyzing Growth:

Growth can be disaggregated into three main components:

Portfolio Momentum: organic revenue growth a company enjoys because of overall expansion in the market segements of its portfolio

Market share performance: organice revenue growth from a company gaining or losing share in a particular market

Mergers and acquisitions: inorganic growth a company achieves when it buys or sells revenues through acquisitions or divestments

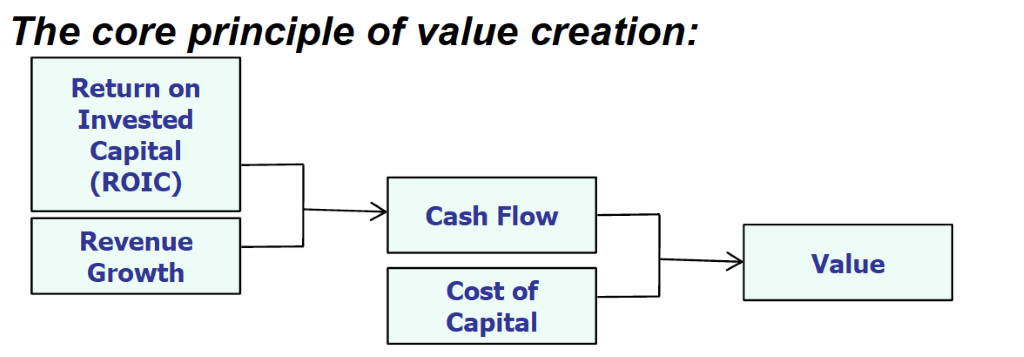

Growth and Value: growth translates to value when return on invested capital (ROIC) exceeds the cost of capital(!!!). Sustaining high growth is much more difficult than sustaining ROIC. Despite some variation on the patterns of growth, high growth is not sustainable, due to the natural cycles of products.

Intrinsic value: the value that WE THINK the company is worth. The actual worth of an investment or asset justified by information about its future cash flows. This is the ‘true’ value according to a model.

Market value: the price determined by buyers and sellers on an open market. It’s the consensus value of all market participants.

Is growth always good? It depends on the return on capital. Growth = IR (investment rate) * ROIC

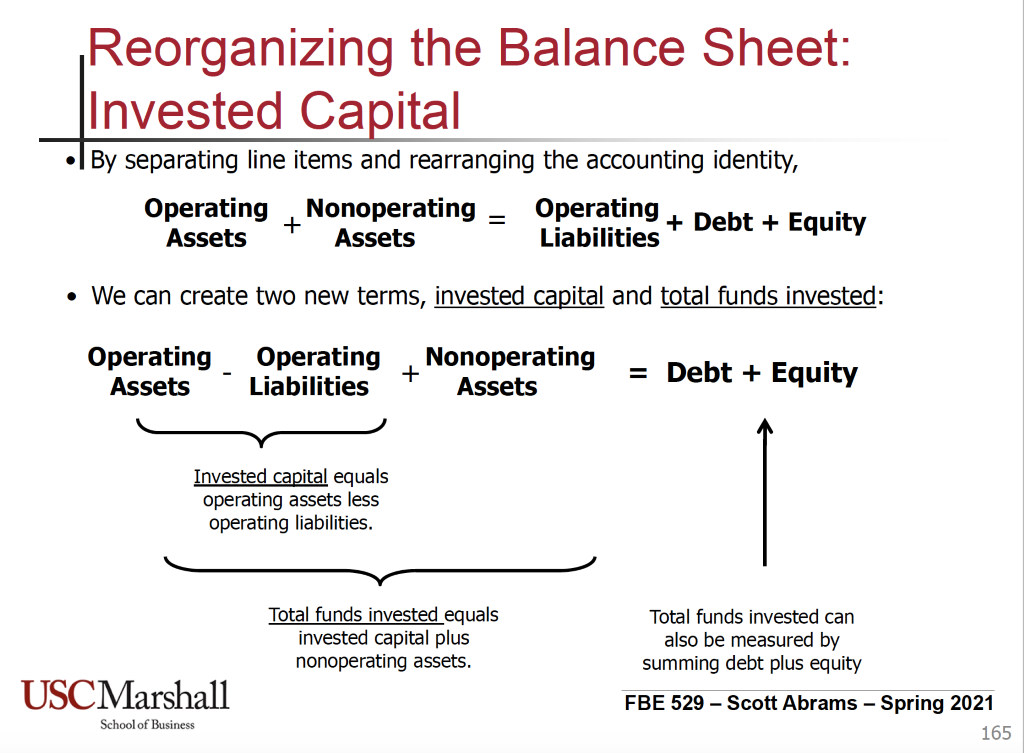

Invested Capital: the cumulative amount that the business has invested in its operations – primarily PP&E and working capital

Guiding Principal of Value Creation

Firms that grow and earn a return of capital that exceeds their cost of capital create value

As long as the spread between ROIC and WACC is positive, new growth creates value. The faster the firm grows, the more value it creates. ROIC > WACC = VALUE CREATION!

If the spread is equal to zero, the firm creates no value through growth. The firm is growing by taking on projects that have NPV of zero

When the spread is negative, the firm destroys value by taking on new projects. If a company cannot earn the necessary return on a new project or acquisition, its market calue will drop. ROIC < WACC = VALUE DESTRUCTION!

High ROIC companies should focus on growth. Low ROIC companies should focus on improving returns before growing.

The amount of value they (the company) create is the difference between cash inflows and the cost of the investment made, adjusted to reflect the fact that tomorrow’s cash flows are worth less than today’s because of the time value of money and the riskiness of future cash flows.

A combination of three primary financial metrics typically measure how well a company is delivering value to shareholders: earnings per share (EPS), return on invested capital (ROIC) or return on equity (ROE), and after-tax cash flow.

Warren Buffet’s principles for an outstanding business:

A high ROIC and is able to reinvest its earnings at a high rate

A “moat”, a barrier against competition, something like a world-class brand or advantage of scale. Often it is the firms business in a particular market

Either an outstanding management or is so powerfully positioned that it doesn’t need one

A large established company might have a low return on capital as it might have lost its competitive advantage (it grew at first thanks to its good ROIC). A small company might have a low return on capital as it struggled to ever establish and source of competitive advantage

A suggested structure for an industry analysis memoSector overview and key players

Industry overview and key players

Breakdown of key sectors within the industry (by revenues) and their associated business models (i.e. – how do they make money?)

For each sub-sector:

Key players

Key financial statistics: market cap, total sales, operating and net profit, margins, risk (beta), recent 5-year equity returns (ROE, ROIC), as well as valuations (P/E, P/S, P/B and EV/EBITDA ratios)

Sector potential short and long term consensus growth rates

Industry features

Sensitivity of sales to the business cycle; Industry life-cycle stage

Operating leverage

Financial leverage

Industry structure: threat to entry, rivalry between existing competitors, pressure from substitute products, bargaining power of buyers, and bargaining power of suppliers

Operating environment: regulatory, political, social, environmental and product risk, trade issues, exchange rate sensitivity, and impact of consolidation and globalization

Industry Trends & Market Outlook for the next 12-36 months? (e.g., how would strong dollar, rising rates, rising commodity costs, or increasing legislation impact the sector?)

Key Financial & Valuation Metrics—Sector specific characteristics (e.g., same store sales for retailers)

Recommendations—Should SIF 2021 overweight or underweight this sector in the next 12-36 months?

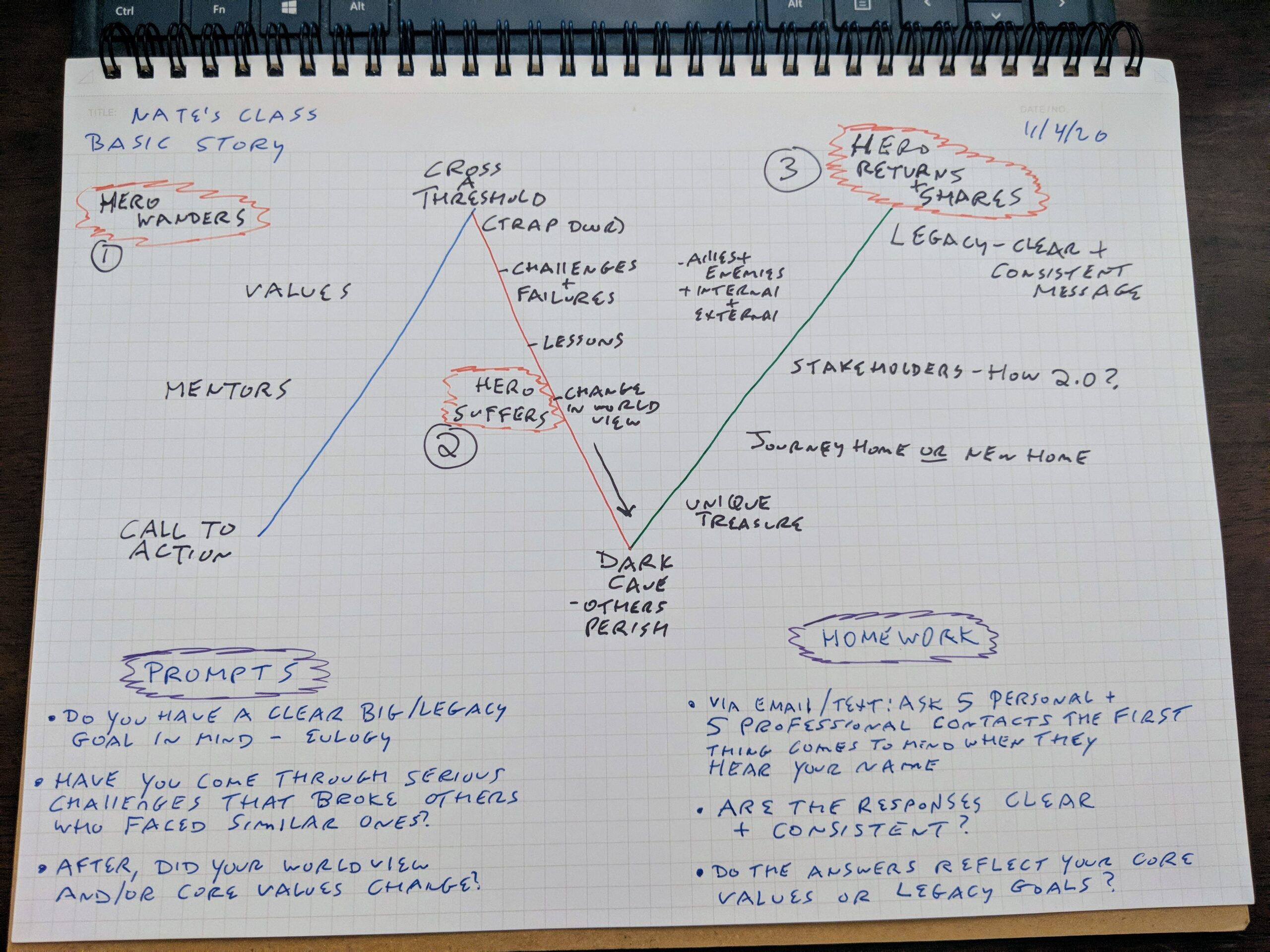

The below is a really nice framework to use when thinking about framing an argument, telling a story, or thinking about your short and long term goals. It can help ensure that arguments are solid, backed by evidence, and are compelling. The next time you need to make an argument, or need to get more clarity around a decision that you need to make.

This framework was introduced to us by Damon D’Amore. He’s an executive mentor and advisor to C-Suite executives and select entrepreneurs and public speakers. Here’s a list of his favorite professional development books:

A quick reminder.. When identifying a problem, we should ask ourselves: what’s going on here…what’s important… what’s less important.. what’s not really important?

The first question strategists should ask is what is the firm trying to do? What do they want to do? From there, it’s important to identify the key sources of success (BTW – A lower price is not a sustainable competitive advantage.